MedSpa Market Overview

FEBRUARY 2024

FEBRUARY 2024

The field of Medical Aesthetics (or “MedSpa”) is dedicated to enhancing patients' cosmetic appearance using a variety of non-surgical methods. What differentiates MedSpas from conventional beauty services and spa treatments is the oversight of qualified medical professionals and licensed estheticians.

Fundamentally, the MedSpa industry is characterized by the availability of non-invasive cosmetic procedures.

In each specified category, a multitude of services are accessible for patient utilization, and these services are becoming increasingly prevalent.

Although pure-play MedSpa practices can administer these services independently, the industry gains added value from diverse medical professionals who integrate these core services into their existing practices.

MedSpas offer a wealth of cosmetic and mental health benefits. The most successful practices blend the confidence associated with high-level medical professionals with the convenience and wellness capabilities of a health spa.

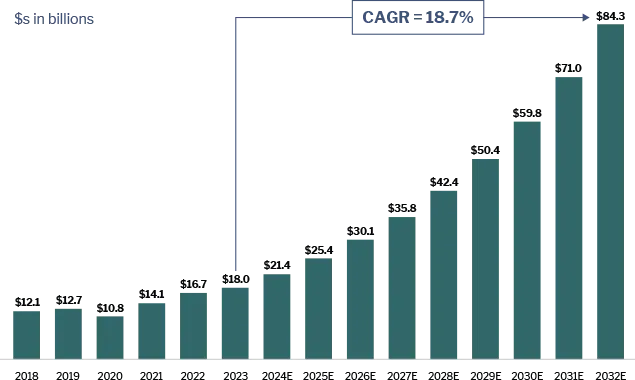

The MedSpa market size reached $18 billion in 2023, with a projected CAGR of 18.7% through 2032. This expansion is fueled by robust consumer trends, highlighted by a heightened focus on wellness and cosmetic care.

The United States dominates the MedSpa market and continues to witness growth. The top four states with the highest concentration of MedSpa businesses are California (11.5%), New York (10.0%), Florida (8.8%) and Texas (7.6%).

Registered MedSpas in the U.S. by the end of 2021.

Registered MedSpas in the U.S. by the end of 2022.

Sources: Expert Market Research, Statistica, Medica Depot, IBISWorld

The demand for non-surgical cosmetic treatments is rapidly increasing. With consumers placing greater emphasis on overall wellness and appearance, there is a growing need for the more affordable and safer procedures that are offered by MedSpa practices.

While the typical consumer remains predominantly female, the number of males seeking aesthetic treatments has tripled since 2000.

The population of adults over 60 is growing and expected to reach 1.4 billion by 2030.

In contrast to traditional medical practices, MedSpas can be owned and operated by a variety of specialized medical professionals. This allows the industry to benefit from core doctors, such as plastic surgeons and dentists, incorporating MedSpa services into their primary business.

Sources: Mordor Intelligence, Data Bridge Market Research

Ownership:

Initial investment:

Recent Acquisitions:

1 Sept 2022

2 Feb 2023

3 Feb 2023

4 Feb 2023

5 April 2023

Ownership:

Initial investment:

Recent Acquisitions:

1 Mar 2023

2 May 2023

3 May 2023

4 Jul 2023

5 Jan 2023

Ownership:

Initial investment:

Recent Acquisitions:

1 Jan 2023

2 Jul 2023

3 Aug 2023

4 Nov 2023

5 Dec 2023

Ownership:

Initial investment:

Recent Acquisitions:

1 Jan 2023

2 Mar 2023

3 May 2023

4 Jun 2023

5 Aug 2023

In the last five years, approximately $3.1 billion in private capital has been invested in the MedSpa industry. These investments are driven by substantial growth and enduring tailwinds, making the MedSpa sector an appealing investment.

Just 8% of MedSpas are under private equity, franchise, or national chains, signaling a substantial opportunity for investors to consolidate the industry.

|

Strong

Growth Catalysts |

Increased demand for core services, rising consumer incomes, an expanding

target

market, technological advancements, and a diverse range of service providers

contributing to significant growth.

|

|

Highly

Fragmented Market |

MedSpa stands out as one of the few healthcare

industries witnessing a faster influx of single-location operators than the

consolidation of existing practices. In 2022, approximately 76% of the U.S.

MedSpa space was dominated by single-location owners, presenting promising

investment opportunities.

|

|

Resilient

Industry |

The industry has proven to be resilient in times of

economic downturn. During the 2008 financial crisis, as well as the COVID-19

pandemic, MedSpa took a hit, but recovered well in the following years.

|

|

Recurring

Nature |

MedSpa practices tend to experience high rates of

returning patients, and the procedures administered are largely recurring in

nature leading to predictable cashflows.

|

|

Demand

Outpacing Supply |

While this issue has not manifested prominently, the

current surge in demand could outpace the supply of qualified medical

professionals. Despite the industry having a varied array of service

providers,

demand is on the rise. Any regulatory measures aimed at expanding the

certifications needed to practice within the industry could pose challenges.

|

Sources: Modern Aesthetics, PitchBook, PR Newswire, BeautyMatter

| Date | Target | Acquirer | Transaction Type | |

|---|---|---|---|---|

| November 2023 | Was acquired by |  |

Platform | |

| October 2023 | Was acquired by | Platform | ||

| September 2023 |  |

Was acquired by |  |

Platform |

| July 2023 |  |

Was acquired by |  |

Platform |

| June 2023 |  |

Was acquired by |  |

Platform |

| May 2023 |  |

Was acquired by |  |

Platform |

| April 2023 |  |

Was acquired by |  |

Platform |

| Date | Target | Acquirer | Transaction Type | |

|---|---|---|---|---|

| January 2024 |

|

Was acquired by |  |

Add-On |

| January 2024 |  |

Was acquired by | Add-On | |

| January 2024 |  |

Was acquired by |  |

Add-On |

| December 2023 |  |

Was acquired by |  |

Add-On |

| December 2023 |  |

Was acquired by |  |

Add-On |

| November 2023 |  |

Was acquired by | |

Add-On |

| November 2023 |  |

Was acquired by |  |

Add-On |

| October 2023 |

|

Was acquired by |  |

Add-On |

| August 2023 |  |

Was acquired by |  |

Add-On |

Rising consumer demand and heightened investor interest in the MedSpa industry has brought about various federal and state regulations, presenting complexities in structuring transactions and establishing new clinics.

CPOM (Corporate Practice of Medicine) Doctrines differ by state, imposing restrictions or outright prohibitions on the ownership of medical practices or businesses by individuals without medical licenses.

As many states classify core MedSpa services as medical practice, non-physician ownership is generally restricted. Investors must consider this when structuring transactions within the MedSpa industry.

Physician and clinic advertising adhere to FTC Act regulations, with consumer information governed by HIPAA. In this visually and digitally focused industry, practitioners must carefully follow these guidelines to avoid penalties for deceptive acts or consumer rights.

in fines per violation (FTC Act)

The AKS and Stark Law bar medical providers from exchanging kickbacks for patient referrals under Medicaid/Medicare. Although most MedSpas operate on a cash basis, those providing treatments like neurotoxin injections for non-cosmetic conditions and participating in federal healthcare programs are subject to these regulations.

states have imposed their own variations (some extending to all cash transactions)

A proposed law in Texas aims to mandate the presence of an NP, PA, or MD on-site for all aesthetics businesses. Additionally, medical directors must be within 75 miles of the business they oversee, and the supervision limit for one MD over NPs and PAs is proposed to decrease from 7 to 5.

The proposed rules restrict estheticians from using blades, performing medical treatments like microdermabrasion and Botox injections, employing devices below the stratum corneum, diagnosing or treating medical conditions, and using lasers or ultrasounds.

Estheticians cannot perform cosmetic medical procedures, unless acting as unlicensed medical assistants under a physician. This restriction would limit estheticians' independent service abilities, affecting the flexibility and efficiency of med spa operations.

The proposed regulation mandates a 90-day notice to the Attorney General (AG) before any health care transactions take effect. The AG reviews based on market competition, quality of care, and access to care, with the authority to approve, conditionally consent, or deny the underlying transaction.

Sources: McGuireWoods LLP, Telos Digital Marketing, Morgan Lewis, Lengea Law, American Med Spa Association, UC Law San Francisco

While federal laws play a role in shaping the regulatory landscape of the MedSpa industry, the crux lies in the diverse regulations of individual states.

| Key Considerations | California | New York | Florida | Texas |

|---|---|---|---|---|

| Does the state have a Corporate Practice of Medicine doctrine? | Yes | Yes | No | Yes |

| Is continued education or advanced training required? | Yes | Yes | Yes | Yes |

| Can you charge commission on laser treatments or injectables? | No | No | No | Yes |

| Can you share profits if you’re not a licensed doctor? | No | No | No | No |

Sources: Dental & Medical Counsel, Facemedical

This document is being provided in connection with an actual or potential mandate or engagement and may not be used or relied upon for any purpose other than as specifically contemplated by a written agreement with the Allen, Mooney & Barnes companies. This document is intended solely for the use of the party to whom it was provided to and is not to be disclosed (in whole or in part), summarized, reprinted, sold, redistributed or otherwise referred to without the prior written consent of the AMB companies.

Allen Mooney & Barnes Brokerage Services is a broker/dealer member of FINRA and SIPC. Allen Mooney & Barnes Investment Advisors, Inc. is an investment adviser registered with the U.S. Securities and Exchange Commission.

Information presented in this document is for informational, educational and illustrative purposes only. While the information in this document is from sources believed to be reliable, the AMB companies make no representations or warranties, express or implied, as to whether the information is accurate or complete and assume no responsibility for independent verification of such information. In addition, the analyses in this document are narrowly focused and are not intended to provide a complete analysis of any matter.

Past performance is not necessarily indicative of future performance. Estimates, projections or indications of future performance can be identified by certain statements, such as “believes,” “expects,” “may,” “will,” “should,” “seeks,” “approximately,” “plans,” “estimates” or “anticipates” or the negative of those words or other comparable terminology, as well as by statements concerning projections, future performance, developments, events, revenues, expenses, earnings, run rates and any other guidance on present or future periods. Any such statements are forward-looking in nature and involve risks and uncertainties. Any statements of future performance are based on assumptions that might not be realized and a number of factors, including without limitation, the volatility of the securities markets, the overall environment for interest rates, risks associated with private equity investments, the demand for public offerings, activity in the secondary securities markets, competition among financial services firms for business and personnel, the effect of demand for public offerings, available technologies, the effect of government regulation and of general economic conditions on our own business and on the business in the industry areas on which we focus and the availability of capital to us. We are under no obligation to update the information presented in this document or to inform you if any such information turns out to be inaccurate or misleading.

The information in this document is not, and is not to be construed as, an offer or a solicitation to buy or sell any securities or any other financial instruments or a recommendation or endorsement to engage in or effect any particular investment or transaction. Moreover, under no circumstances should the information in this document be considered legal, tax or accounting advice or relied upon, therefore. The recipient is advised to rely on the advice of its own professionals and advisors for such matters and should make an independent analysis and decision regarding any transaction based upon such advice.

The information in this document is not intended for distribution to, or use by, any person or entity in any jurisdiction or country where such distribution or use would be contrary to law or regulation or for any distribution or use that would subject the AMB companies to any registration requirement within such jurisdiction or country.

AMB focuses on lower middle-market healthcare niches where consumerism and fragmentation meet to disrupt traditional healthcare channels. We typically advise companies with EBITDA of $5M to $20M and an average enterprise value of $100M, but will move up and down the spectrum. AMB’s research-oriented approach to business development has resulted in a vast network of strategic and financial sponsor relationships that yield industry leading intelligence and optimal outcomes for our clients.

Managing Director

843-501-2183 Direct

mikel.parker@ambadvisors.com

Managing Director

843-405-1108 Direct

ryan.loehr@ambadvisors.com

Vice President

843-371-8596 Direct

johnny.cross@ambadvisors.com

Senior Associate

843-473-7981 Direct

kevin.williams@ambadvisors.com

Associate

843-576-4709 Direct

sully.hagood@ambadvisors.com

Analyst

843-405-1112 Direct

josh.hall@ambadvisors.com

Analyst

405-343-1643 Direct

asha.hamaker@ambadvisors.com